Mitch Finnen | Private Wealth Advisor

May 18th, 2026

Treasurer Jim Chalmers handed down the 2026-2027 budget last week, setting the proverbial cat amongst the pigeons. The budget will result in a substantial change to the way portfolios and wealth are organized over the coming years, if it passes through the senate unchanged.

While the budget has minimized the role of some existing tax structures, it has, in leaving other environments unchanged, emphasized their role substantially.

I wanted to give an update, and quick examination, of where the predominant changes are from a private wealth perspective. Notably, we do not manage residential or negatively geared property on behalf of clients and as such commentary on these specific changes is better sourced elsewhere.

Please note that none of the below is tax advice – merely a prompt to speak with a registered tax practitioner if you believe you may be impacted. Any modelling is presented ceteris paribus without consideration of your personal position.

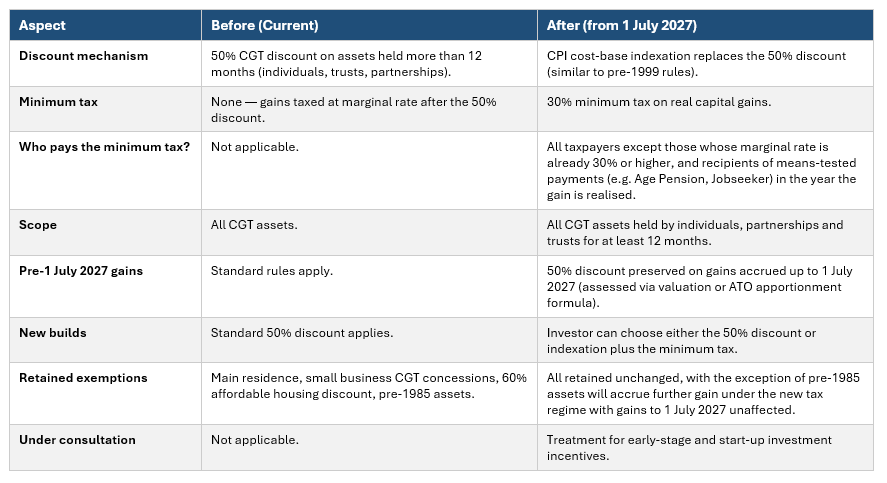

From 1 July 2027, the 50% capital gains tax (CGT) discount will be replaced by cost base indexation for assets held for more than 12 months, together with a 30% minimum tax on net capital gains, for individuals, trusts and partnerships.

This change will also apply to pre-1985 CGT assets, but with the changes only applying to gain made beyond 1 July 2027.

The largest impact here will be on individuals and trusts engaging in high-growth investing, where they expect more rapid growth of assets or to substantially exceed the rate of inflation in the long run. The 50% discount was a powerful mechanism that typically capped CGT at 22.5% - now, the minimum will be 30% and the maximum will be the highest marginal tax rate less the inflation on the asset.

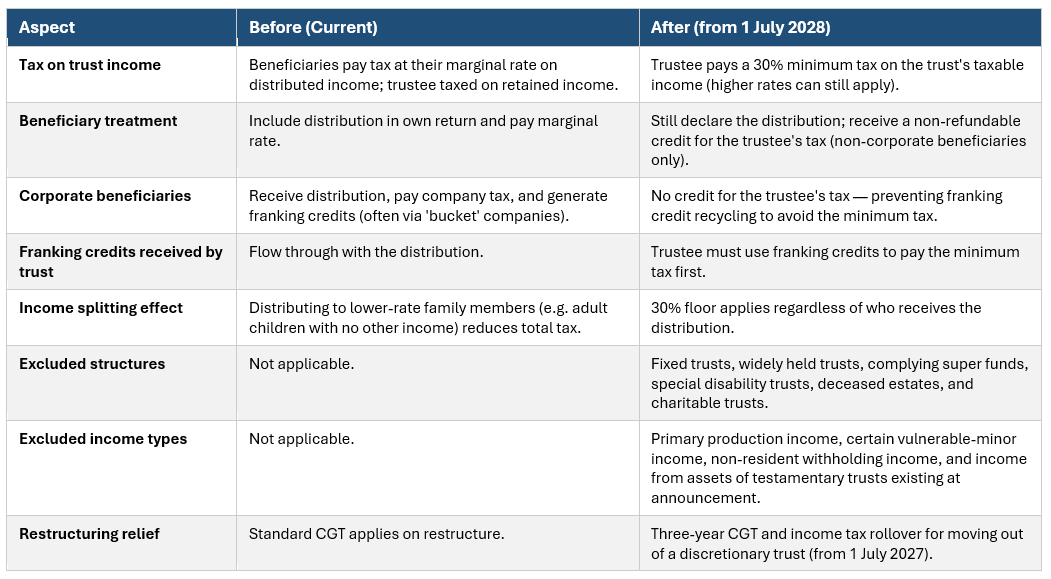

This change has negated two very popular tax deferral/minimization strategies –distributing to a bucket company and distributing to adult children on lower tax rates.

Under the current legislation, there is no minimum tax level applied to a discretionary trust. The income or gain can be streamed to specific beneficiaries, who then pay their marginal tax rate on income and gain received from the trust. No additional top-up is required. Under the new regime, beneficiaries will receive a non-refundable tax credit for the tax paid by the trust. This can be applied against their own income tax liability (to prevent double taxation). If their marginal rate is below 30%, the credit reduces to zero and the prevailing rate remains at 30%.

Income and realized gain can also be streamed directly to a bucket company, where 30% tax on this distribution is paid at the trustee level, and a further round of tax is then applied to the bucket company making the effective tax rate 51% at the corporate level. When streaming on to the individual, the current legislation would have an effective tax rate of 62.9% once distributed to an individual at the highest marginal tax rate. If any changes are to be applied, we expect this is a likely candidate for reform when this moves from budget paper to legislation before parliament.

We are also carefully watching how rollover relief is structured – this will impact many people who wish to move their affairs into a company.

The treatment for corporate beneficiaries appears to be different and further detail is expected as we progress through a consultancy period. At first glance, it appears the measures are intended to prevent the minimum tax being circumvented by cycling income through a ‘bucket’ company. For example, corporate beneficiaries will not receive non-refundable credits for tax payable by the trustee, to avoid them converting these to refundable franking credits to avoid the minimum tax. In practice today, this means that the income would be taxed at the trustee level, and then again as income received for the company.

Just this measure taken alone will mean substantial change to the landscape.

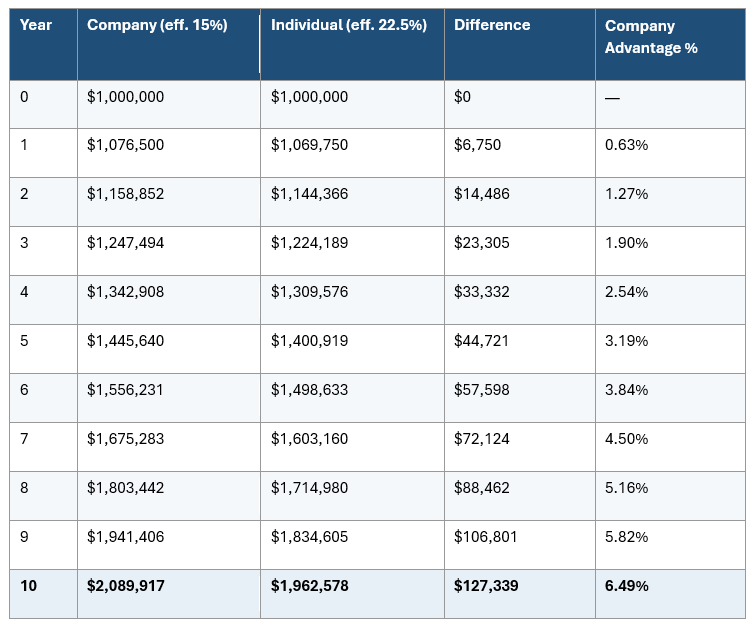

Companies have two major advantages in the new environment: The first is that their maximum tax rate now matches the minimum tax rate at 30%. The second is the ability to retain earnings, and compound on the difference between 30% and the marginal tax rate for directors/shareholders until top-up tax is required upon dividend issuance.

An example of a $1M portfolio growing at 9% with 50% turnover per annum is below. Please note tax rates account for the turnover, e.g. half the portfolio turned over equals half of all the gains being realized:

While a corporate entity cannot reduce the tax on funds eventually distributed, the compounding on what otherwise would have been paid makes a substantial difference over a decade.

Nothing yet– changes are yet to be finalized and approved as legislation. We must wait and see what the final budget looks like. If the changes hold in their current form, the below are likely knock-on effects. If you feel as though you would like to discuss these changes, please reach out to EW&L for a confidential consultation on how we can assist you.

CGT concessions were left intact within the Super environment. This means that in Super, you will pay 15% on income and short-term capital gain, and 10% on long-term capital gain. A natural response will be to house high-growth, high turnover asset classes within super at greater rates.

Investment companies will become more prevalent through time, as discretionary trusts become less attractive environments. The ability to retain earnings on the balance sheet is especially attractive.

These changes will push investors to review how best to utilize their capital in markets. In our view, this is the time to revisit alternative asset managers, property trusts (especially commercial office), and the structuring of your ‘higher growth’ investments, especially as we approach 1 July 2027.

Emanuel Whybourne & Loehr Pty Ltd (ACN 643 542 590) is a Corporate Authorised Representative of EWL PRIVATE WEALTH PTY LTD (ABN: 92 657 938 102/AFS Licence 540185).Unless expressly stated otherwise, any advice included in this email is general advice only and has been prepared without considering your investment objectives or financial situation.

There has been an increase in the number and sophistication of criminal cyber fraud attempts. Please telephone your contact person at our office (on a separately verified number) if you are concerned about the authenticity of any communication you receive from us. It is especially important that you do so to verify details recorded in any electronic communication (text or email) from us requesting that you pay, transfer or deposit money, including changes to bank account details. We will never contact you by electronic communication alone to tell you of a change to your payment details.

This email transmission including any attachments is only intended for the addressees and may contain confidential information. We do not represent or warrant that the integrity of this email transmission has been maintained. If you have received this email transmission in error, please immediately advise the sender by return email and then delete the email transmission and any copies of it from your system. Our privacy policy sets out how we handle personal information and can be obtained from our website.

The information in this podcast series is for general financial educational purposes only, should not be considered financial advice and is only intended for wholesale clients. That means the information does not consider your objectives, financial situation or needs. You should consider if the information is appropriate for you and your needs. You should always consult your trusted licensed professional adviser before making any investment decision.

Emanuel Whybourne & Loehr Pty Ltd (ACN 643 542 590) is a Corporate Authorised Representative of EWL PRIVATE WEALTH PTY LTD (ABN: 92 657 938 102/AFS Licence 540185).Unless expressly stated otherwise, any advice included in this email is general advice only and has been prepared without considering your investment objectives or financial situation.

There has been an increase in the number and sophistication of criminal cyber fraud attempts. Please telephone your contact person at our office (on a separately verified number) if you are concerned about the authenticity of any communication you receive from us. It is especially important that you do so to verify details recorded in any electronic communication (text or email) from us requesting that you pay, transfer or deposit money, including changes to bank account details. We will never contact you by electronic communication alone to tell you of a change to your payment details.

This email transmission including any attachments is only intended for the addressees and may contain confidential information. We do not represent or warrant that the integrity of this email transmission has been maintained. If you have received this email transmission in error, please immediately advise the sender by return email and then delete the email transmission and any copies of it from your system. Our privacy policy sets out how we handle personal information and can be obtained from our website.

NewsLetter

Free Download